The European softwood industry is navigating a period of gradual stabilization after three years of difficult market conditions, according to outlooks presented at the 73rd International Softwood Conference in Oslo in October 2025. While both producers and traders report modest improvements, the sector faces continuing challenges, including record-high log prices, limited spruce availability, and subdued construction activity across key markets.

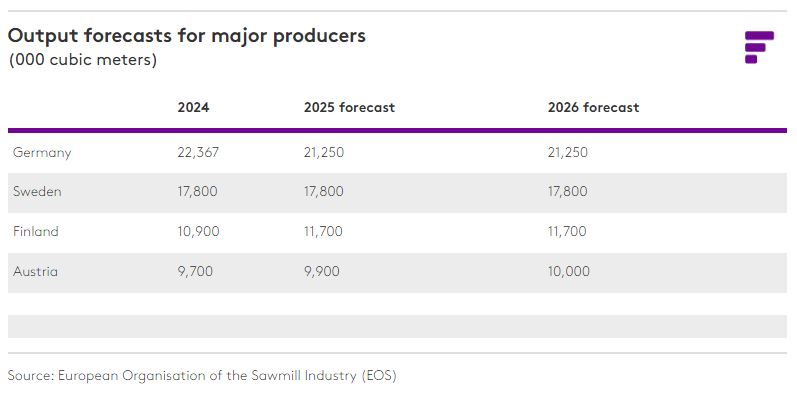

European softwood sawmill production has plateaued at approximately 78 million cubic meters per year across European Organisation of the Sawmill Industry (EOS) member countries since 2023, representing a 10% decline from the 2021 peak of 86 million cubic meters, according to EOS President Tommi Sneck. When including all EU countries plus Norway and Switzerland, total production reaches 97 million cubic meters.

-

That’s a remarkable amount of work hours for a single machine, the Norcar 600 owned by Erkki Rinne is taken well care of, it even has the original Diesel engine.

-

Kieran Anders is a forestry contractor working in the lake district. His work involves hand cutting and extracting timber using a skidder and tractor-trailer forwarder.

-

It is not possible to eliminate chain shot, but there are simple steps that can be taken to reduce the risk.

-

Arwel takes great pride in the fact that the mill has no waste whatsoever, “the peelings are used for children’s playgrounds, gardens and for farm animals in barns in the winter and the sawdust has multiple uses in gardens and farms as well.

-

Timber hauliers need to encourage young blood in, and also look after the hauliers we have, we need make the sector a safe and positive place to work.

FIND US ON

“After peaking in 2021, production in the EOS countries declined significantly over the last few years to adjust to the demand decline,” Sneck told conference attendees. “Since 2023, in the EOS countries overall, production is stable at around 78 million cubic meters on levels lower than the period before the pandemic.”

Country-level data reveals varied performance across Europe’s major producing nations:

Germany has experienced the steepest production decline from 2021 peaks, while Finland shows recovery with a forecast increase to 11.7 million cubic meters in 2025. Austria, Sweden and, among smaller producers, Latvia and Norway, have largely stabilized their output levels.

Consumption shows marginal growth

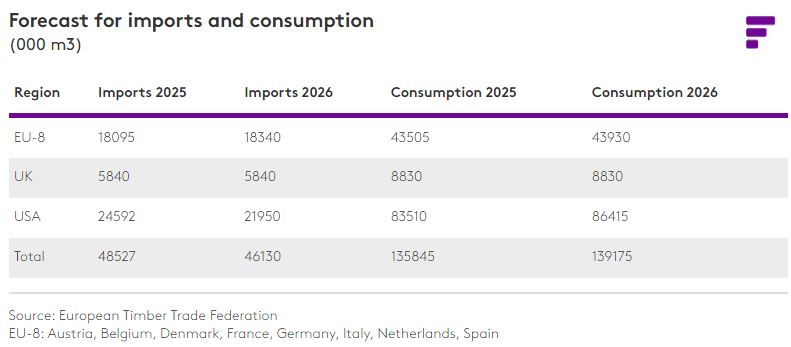

On the demand side, sawn softwood consumption across EOS member countries plus the UK increased by 2.1% in 2024 to reach 42.8 million cubic meters, still 13% below 2021 levels. The European Timber Trade Federation (ETTF) forecasts consumption will edge upward to 43.5 million cubic meters in 2025 and 43.9 million cubic meters in 2026.

“For the third consecutive year, the first two quarters of 2025 offered hope in some European countries with increasing exports and European consumption – slightly and from a relatively low basis,” Sneck noted. “The summer was disappointing and the feeling across the industry is that the next few months will not be great.”

Import volumes tell a similar story of modest recovery. Total imports to major European markets reached 48.2 million cubic meters in 2024, up by 5.4% from forecasts made the previous year. For 2025, ETTF Vice-President Morten Bergsten projects imports of 48.5 million cubic meters, with a slight decline to 46.1 million cubic meters in 2026, driven primarily by reduced US imports.

Raw materials prices squeeze profitability

A critical challenge facing European sawmillers is the dramatic increase in raw materials costs, particularly in Nordic countries where log prices have reached record highs. In Finland, the spruce log price index has risen to approximately 160 (base 2015=100), while sawn spruce prices have increased to only about 150, creating a significant margin squeeze.

“Sawnwood prices have grown but they have not kept pace with the increase of log prices, which is one of the main reasons for the low profitability of the industry,” Sneck emphasized. “The increase in log prices took place in the middle of weak demand for wood. What will happen when demand resumes?”

The situation differs somewhat in Central Europe, where prices haven’t risen as sharply as in the north but remain high compared with global competitors. A notable price gap has emerged between fresh logs and beetle-damaged logs in countries like Germany and the Czech Republic.

Spruce scarcity reshapes supply dynamics

Looking ahead, spruce availability is emerging as a structural constraint on European production. Germany’s spruce stocks are projected to decline dramatically from 1.2 billion cubic meters in 2012 to just 300 million cubic meters by 2100, according to data presented at the conference. The Czech State Forests harvest has stabilized at around 8 million cubic meters per year after peaking above 14 million cubic meters in 2020 during the bark beetle crisis.

“Due to climate change and its relative lack of suitability in a warming climate, availability of spruce logs will decline in the next few decades,” Sneck warned. “We already see the first effects with reduced availability of spruce logs in the aftermath of the bark beetle crisis a few years ago.”

This scarcity is driving mills in Central Europe and southern Sweden to increase their use of pine as an alternative. From a structural perspective, pine and spruce often meet the same strength classification grades, though they differ in appearance, handling, and treatment performance.

“The industry should do more to also promote pine as a structural timber, as the share of pine in production will increase compared with spruce,” Sneck urged.

Construction sector shows signs of bottoming out

The construction downturn that began in 2022 appears to have reached its nadir. EU building permits for new dwellings declined by 15% in floor area in 2023 and by a further 2% in 2024, with the dwelling index stagnating last year. However, recent monthly data show permits may have bottomed out and are displaying slight improvement.

“Confidence in the construction sector is still quite low but the issuance of building permits for new houses in the EU has reached its lowest point and is displaying slight improvement,” Sneck observed. “Yet, the granting of permits is still very low compared with 2021, especially in Central Europe.”

Large markets with traditionally high wood consumption have been particularly hard hit, with Germany, France, Finland, and Austria all experiencing significant permit declines. Spain stands out as a positive outlier with expanding construction activity.

Bergsten’s outlook for individual markets reveals mixed conditions:

Germany: Gradual rebound expected, driven by public works and energy renovation

France: Moderate recovery supported by green transition and increasing building permits

Spain: Strong expansion continues, fueled by housing deficit and renovation activity

Italy: Stabilizing with a potential small decline as PNRR (recovery plan) stimulus winds down

Netherlands: Growing market driven by bio-based building policies

Denmark: Moderate recovery linked to green transition and lower interest rates

Despite these challenges, wood construction continues to gain market share. In Germany, the share of new residential building permits using wood as the predominant material reached 24.1% in 2024, up from 20.4% in 2020. Swedish data shows similar trends in multi-dwelling buildings, where wood’s share has risen from around 10% in the mid-2000s to 15-16% in recent years.

Export markets provide mixed picture

EU exports of sawn softwood to non-EU markets totaled €6.5 billion in 2024 ($7.48bn), up by 13% in the first half of 2025 compared with the same period in 2024. The US remains the largest single destination outside Europe, accounting for over 16.5% of extra-EU exports, followed by Japan (9.4%) and Egypt (6.4%).

However, China’s share has collapsed to just 2.2% as deliveries fell by 37% in the first half of 2025 to only €85 million. The UK, while technically outside the EU, can be considered part of the European market and accounts for 26% of non-EU deliveries.

“In H1 2025, shipments to the US increased by 19% to €620 million, to Japan they declined by 7% to €350 million,” Sneck reported. “Deliveries to Egypt grew by 8% to €240 million, while deliveries to China went down by 37% to just €85 million.”

The US market outlook includes a forecast 10.7% decline in imports for 2026 to 22 million cubic meters, though domestic consumption is expected to rise by 3.5% to 86.4 million cubic meters, suggesting increased domestic production will fill the gap.

Russian competition persists in key markets

Russian lumber production has also declined from pandemic-era peaks, stabilizing at around 28 million cubic meters annually, down from over 32 million cubic meters in 2021. Russian exports have fallen by approximately 40% since 2019 to 18.7 million cubic meters in 2024.

China absorbs about 60% of Russian exports (11.2 million cubic meters in 2024), though these volumes declined by 10% year over year in the first half of 2025 as Chinese market prices remained depressed. Russia is redirecting volumes to MENA (Middle East and North Africa) and CIS countries, with an estimated 1.7 million cubic meters shipped to MENA in 2024, including 550,000 cubic meters to Egypt.

Notably, Russia still exports sizable quantities to Japan, maintaining a presence in this important market despite EU sanctions on Russian timber.

Industry calls for policy support

Both presenters emphasized the need for supportive policy frameworks to enable recovery and address structural challenges. Sneck highlighted the tension between sustainability regulations and supply availability.

“We need to fight in Brussels and at the national level to show policymakers that if we are serious about decarbonization, European forests should not be seen as ‘green museums’ but also as essential providers of wood,” he argued. “So, policies need to reflect this.”

The presentations referenced numerous regulatory frameworks affecting the sector, including the EU Timber Regulation (EUTR), EU Deforestation Regulation (EUDR), and various certification schemes (FSC, PEFC, DGNB ratings for buildings).

Bergsten struck a cautiously optimistic note about the sector’s direction: “Europe is on the path to recovery, and our business – our trade, our industry – is looking ahead to a slightly more positive 2026. Despite many uncertainties, especially on the political and regulatory level, wood remains the future–naturally.”

Outlook: cautious optimism

The consensus outlook for 2025-2026 reflects modest improvement from a low base, with consumption forecast to increase by approximately 2.5% compared with 2024 levels. However, this growth remains well below what would be needed to support an accelerated green transition in European construction.

“In the short term the situation will remain difficult for the European wood industry,” Sneck concluded. “There is renewed hope for 2026, but the industry has already been disappointed over the last couple of years.”

Key questions for the sector include whether construction markets have truly bottomed out, whether the second half of 2026 will bring stronger recovery, how the industry will adapt to reduced spruce availability, and whether log prices will moderate to restore profitability.

With Europe having underbuilt housing for nearly 20 years, increasing renovation requirements for energy efficiency, and wood’s growing market share as a building material, the fundamentals suggest potential for stronger growth. Whether 2026 marks the turning point remains to be seen, but both producers and traders are positioning for gradual improvement while managing continuing structural challenges.

Source: fastmarkets.com

Sign up for our free monthly newsletter here

Contact forestmachinemagazine@mail.com to get your products and services seen on the world’s largest professional forestry online news network.

#homeoflogging #writtenbyloggersforloggers #loggingallovertheworld

Written by loggers for loggers and dedicated solely to the equipment used in forestry operations.